Setting a budget is one of those life skills that sounds simple but can feel overwhelming when you dive into it. Whether you’re managing your personal finances, running a small business, or handling a household, creating a budget is like building a roadmap for your money. It helps you decide where your dollars should go, plan for the future, and avoid financial stress. But here’s the catch: not everything should influence your budgeting decisions. Some factors can throw you off track, leading to unrealistic plans or unnecessary spending. In this article, we’ll explore what you shouldn’t consider when setting a current budget, why these factors can derail your financial goals, and how to focus on what truly matters.

This guide is written in a friendly, human tone to make it easy to read and understand for everyone—whether you’re a teenager saving for a new gadget, a young professional juggling bills, or a retiree planning for the years ahead. Let’s break it down step by step and include a handy table for quick reference.

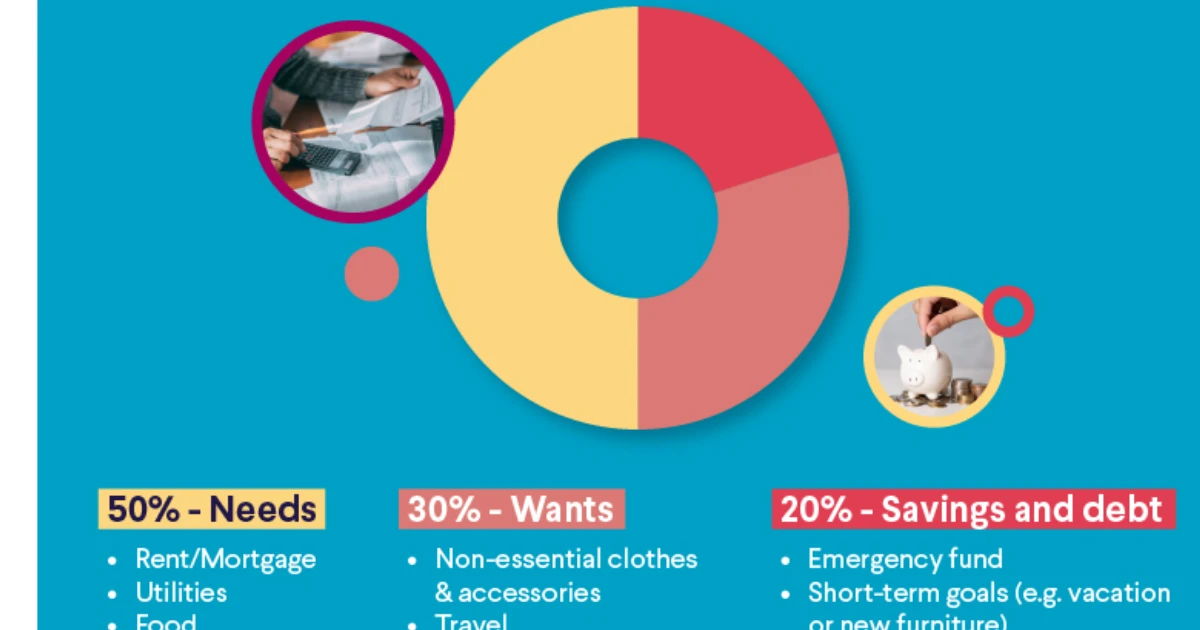

Why Budgeting Matters

Before we dive into what to avoid, let’s talk about why budgeting is so important. A budget is like a GPS for your finances. It helps you:

-

Track your income and expenses: Know exactly how much money is coming in and going out.

-

Plan for goals: Save for a vacation, a new car, or retirement without stress.

-

Avoid debt: Prevent overspending and reliance on credit cards.

-

Prepare for emergencies: Build a safety net for unexpected expenses, like medical bills or car repairs.

But to make a budget that works, you need to focus on the right factors. Including irrelevant or misleading information can mess up your plan, leaving you frustrated or financially strained. So, let’s explore what you shouldn’t consider when setting your budget.

What Should Not Be Considered Which of the Following Should Not Be Considered When Setting a Current Budget?

When creating a budget, it’s tempting to factor in everything that crosses your mind. But some things are better left out. Here are the key factors you should avoid and why they don’t belong in your budgeting process:

1. Unrealistic Income Projections

It’s easy to get excited about potential income, like a big bonus, a side hustle that might take off, or an investment that could pay dividends. But banking on money that isn’t guaranteed is a recipe for trouble. When setting your budget, stick to your current, reliable income. This includes your salary, regular freelance payments, or any consistent revenue stream.

Why to avoid it: If you base your budget on income that doesn’t materialize, you’ll overspend and struggle to cover essentials. For example, if you assume you’ll get a $5,000 bonus and plan your budget around it, but the bonus never comes, you could end up in debt or dipping into savings.

What to do instead: Use your take-home pay or guaranteed income as the foundation. If extra money comes in, treat it as a bonus and allocate it to savings, debt repayment, or a fun splurge after it arrives.

2. Other People’s Lifestyles

In the age of social media, it’s hard not to compare yourself to others. You see friends posting about their fancy vacations, new cars, or designer clothes, and you might feel pressured to keep up. But their lifestyle shouldn’t influence your budget. Everyone’s financial situation is unique, and copying someone else’s spending habits can lead to overspending or neglecting your own goals.

Why to avoid it: Trying to match someone else’s lifestyle can push you to spend beyond your means. For instance, if your neighbor buys a luxury SUV, you might feel tempted to upgrade your car, even if it stretches your finances thin. This can lead to debt or derail your savings goals.

What to do instead: Focus on your own financial priorities. Ask yourself: What are my goals? Do I want to save for a house, pay off student loans, or build an emergency fund? Let those priorities guide your budget, not someone else’s Instagram feed.

3. Temporary Discounts or Sales

Who doesn’t love a good deal? Sales, limited-time offers, and discounts can be tempting, but they shouldn’t dictate your budget. Just because something is on sale doesn’t mean you need to buy it. Including temporary discounts in your budget can lead to impulse purchases that eat into funds meant for essentials or savings.

Why to avoid it: Sales can trick you into thinking you’re saving money when you’re actually spending unnecessarily. For example, if you budget $200 for clothes because of a “buy one, get one free” sale, you might end up buying items you don’t need, just to take advantage of the deal.

What to do instead: Stick to a budget based on your needs, not external promotions. If a sale aligns with something you already planned to buy (like replacing worn-out shoes), great! But don’t let discounts drive your spending decisions.

4. Past Spending Mistakes

We’ve all made financial missteps—maybe you splurged on a gadget you rarely use or racked up credit card debt during a tough month. While it’s important to learn from those mistakes, they shouldn’t dictate your current budget. Focusing on past errors can make you overly cautious or lead to guilt-driven decisions that aren’t practical.

Why to avoid it: If you’re fixated on past overspending, you might cut your budget too drastically in areas like groceries or healthcare, which can harm your quality of life. Alternatively, you might think, “I’ve already messed up, so why bother?” and give up on budgeting altogether.

What to do instead: Start fresh with a realistic budget based on your current income, expenses, and goals. If you have debt from past mistakes, include a manageable repayment plan in your budget, but don’t let guilt or regret shape your entire financial plan.

5. Short-Term Trends or Fads

Trends come and go—whether it’s the latest tech gadget, a trendy diet, or a hot investment opportunity. Including these in your budget can lead to wasteful spending on things that lose their appeal quickly. For example, spending hundreds on a trendy fitness gadget might seem like a good idea now, but if it’s collecting dust in six months, it wasn’t worth the budget space.

Why to avoid it: Fads are often expensive and short-lived. Budgeting for them can divert money from long-term priorities, like saving for retirement or paying off a mortgage. Plus, trends can create a cycle of chasing the next big thing, which is unsustainable.

What to do instead: Focus on timeless needs and goals. If a trendy item aligns with your values or long-term plans (like a fitness tracker that supports your health goals), consider it carefully, but don’t let hype drive your budget.

6. Overly Optimistic Expense Cuts

When creating a budget, it’s tempting to slash expenses to the bone to free up more money for savings or debt repayment. But assuming you can live on a bare-bones budget forever is unrealistic. For example, budgeting $50 a month for groceries when you typically spend $300 is setting yourself up for failure.

Why to avoid it: Overly optimistic cuts can make your budget unsustainable, leading to frustration or abandoning the plan altogether. You might also deprive yourself of essentials, like healthy food or necessary utilities, which can harm your well-being.

What to do instead: Be realistic about your expenses. Look at your spending habits over the past few months to understand your true costs. Then, find reasonable areas to cut back, like eating out less or canceling unused subscriptions, without sacrificing your quality of life.

Quick Reference Table: Which of the Following Should Not Be Considered When Setting a Current Budget?

|

Factor to Avoid |

Why It’s a Problem |

What to Do Instead |

|---|---|---|

|

Unrealistic Income Projections |

Leads to overspending if expected income doesn’t materialize. |

Base your budget on guaranteed, current income. |

|

Other People’s Lifestyles |

Encourages spending beyond your means to “keep up.” |

Focus on your own financial goals and priorities. |

|

Temporary Discounts or Sales |

Promotes impulse buys that may not align with your needs. |

Stick to planned purchases, using sales only when they fit your budget. |

|

Past Spending Mistakes |

Can lead to guilt-driven or overly restrictive budgets. |

Start fresh with a realistic budget and include debt repayment if needed. |

|

Short-Term Trends or Fads |

Diverts money from long-term goals to fleeting purchases. |

Prioritize timeless needs and evaluate trends carefully. |

|

Overly Optimistic Expense Cuts |

Creates unsustainable budgets that lead to frustration. |

Use past spending as a guide and make reasonable cuts. |

Common Budgeting Mistakes to Watch Out For

Beyond the factors above, here are a few other pitfalls to avoid:

-

Ignoring Small Expenses: That daily coffee or streaming subscription might seem minor, but small expenses add up. Track them to see their true impact.

-

Forgetting Annual Costs: Expenses like car insurance or property taxes can sneak up if you don’t budget for them monthly.

-

Not Communicating with Others: If you share finances with a partner or family, make sure everyone’s on the same page to avoid conflicts.

Real-Life Example: Sarah’s Budgeting Journey

Let’s bring this to life with a quick story. Sarah, a 30-year-old teacher, wanted to save for a down payment on a house. When she first created her budget, she made a few mistakes:

-

She assumed she’d get a summer tutoring gig and budgeted based on that extra income.

-

She saw her friend’s new furniture and allocated money for a similar upgrade.

-

She slashed her grocery budget to $100 a month, thinking she could “make it work.”

Within two months, Sarah was stressed. The tutoring gig fell through, she didn’t need the furniture, and she was tired of eating instant noodles. After learning what not to consider, she revised her budget:

-

She used only her teaching salary.

-

She ignored her friend’s purchases and focused on her house goal.

-

She set a realistic grocery budget of $250 based on past spending.

Six months later, Sarah was saving $400 a month toward her down payment and felt in control of her finances.

Why Avoiding These Factors Leads to Financial Success

By steering clear of these budgeting pitfalls, you set yourself up for success. You’ll create a plan that’s realistic, sustainable, and aligned with your goals. Avoiding unrealistic income projections keeps you grounded. Ignoring other people’s lifestyles lets you focus on what matters to you. Skipping temporary sales and trends prevents wasteful spending. And letting go of past mistakes gives you a fresh start.

A good budget empowers you to take control of your money, reduce stress, and work toward your dreams—whether that’s a new home, a dream vacation, or a secure retirement.

Final Thoughts

Setting a budget doesn’t have to be complicated, but it does require focus. By avoiding factors like unrealistic income, social pressures, or fleeting trends, you can create a budget that’s practical and effective. Use the table above as a quick guide, and remember to prioritize your own income, expenses, and goals. With a little discipline and regular check-ins, you’ll be on your way to financial confidence.